Opportunities for U.S. Consumer-Oriented Products in Chile

Contact:

Link to report:

Executive Summary

Chile remains the largest South American consumer-oriented market for U.S. exporters. Increasing wealth, lower barriers to entry, and the modern Chilean economy present opportunities for increased agricultural trade as COVID-19 restrictions and social-political tensions ease. This economic recovery has also attracted increased competition, especially from the European Union, Brazil, and Argentina; but premium U.S. products including beer, distilled spirits, pork and pork products, cheese, and specialty beef cuts hold potential for Chilean growth in the retail sector as well as the hotel, restaurant, and institutional sector.

Macroeconomic Perspective

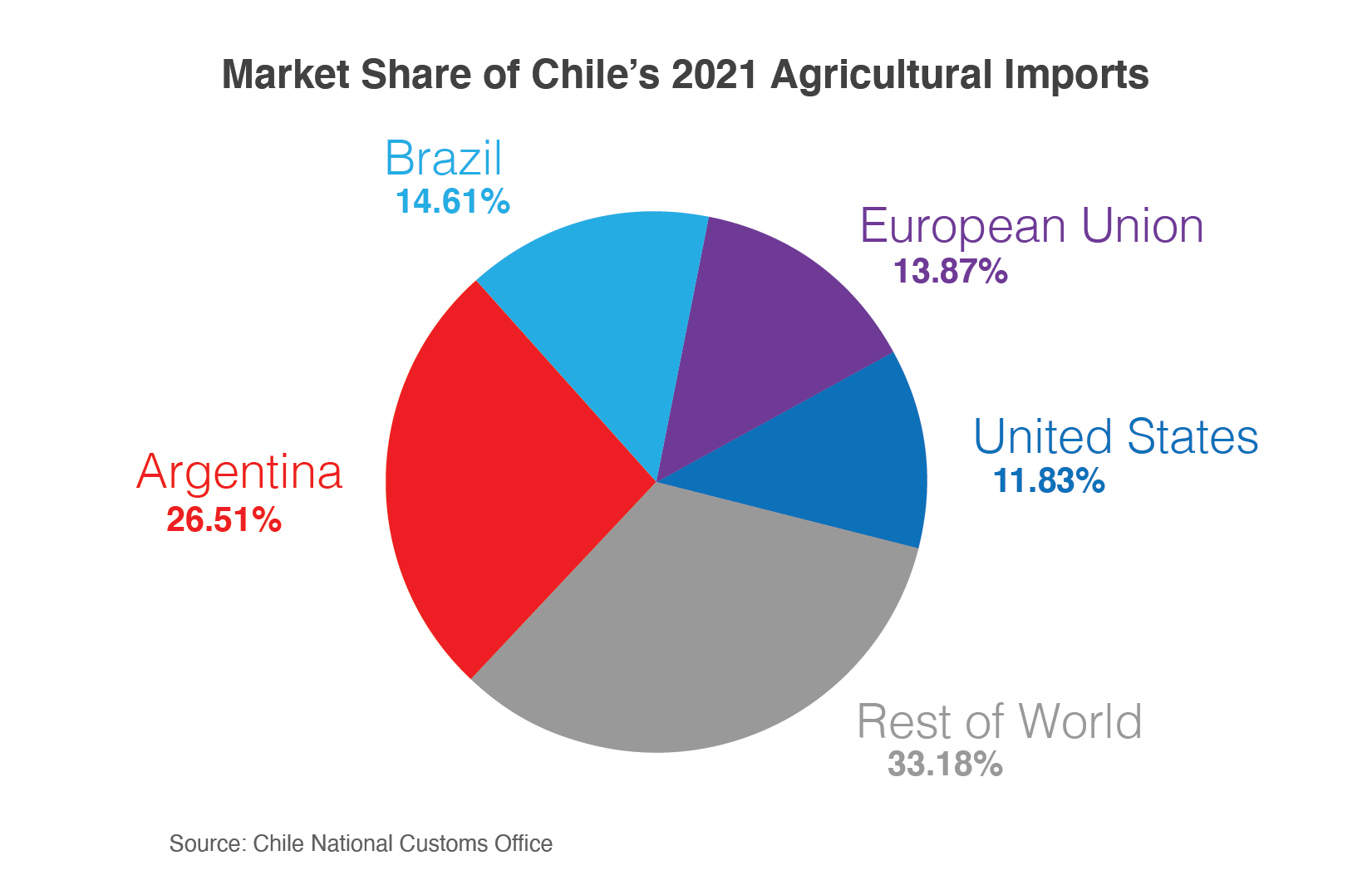

During 2021, the United States became Chile’s fourth-largest supplier of agricultural products after Argentina, Brazil, and the European Union (EU).1 Both Brazil and the EU overtook U.S. agricultural exports to Chile, as they increased their total agricultural export values by 55 and 65 percent, respectively. Top U.S. products exported to Chile in 2021 were beer ($178.2 million), feeds and fodders ($143.7 million), pork and pork products ($111.4 million), dairy products ($105.6 million), and beef and beef products ($94.8 million).

Although Chile has a relatively small population of 19.7 million people, it is the second-largest market in South America for U.S. agricultural products after Colombia, and the largest South American market for U.S. consumer-oriented agricultural products ($886.4 million in 2021). With an easing of COVID-19 restrictions and the stabilization of the country’s social-political tensions, Chile’s gross domestic product (GDP) rose by 12 percent in 2021. The Chilean Central Bank projects a 1.5 to 2.5 percent GDP growth rate for 2022. Throughout this time, Chile has maintained the highest per capita GDP, adjusted for purchasing power parity, in South America.

Consumption Trends and Market Drivers

The Office of Agricultural Affairs (OAA) at the U.S. Embassy in Santiago reports that Chileans remain price sensitive following the economic slowdown. At the same time, foreign import competition has increased in several product categories, particularly in cheese and beer imports from the EU, pork products from the EU and Brazil, and beef products from Brazil and Argentina.

According to Euromonitor, Chilean supermarkets comprise the majority of the country’s food retail industry, recording a 7-percent sales increase in 2021 to $7.8 million. Large grocery chains, including Unimarc, are increasingly offering a wider range of health-conscious products due to consumer demand for natural foods. The hotel, restaurant, and institutional (HRI) sector also saw important rebound growth, increasing by 38 percent in 2021. However, restaurants serving North American cuisine drove that recovery and outperformed all other categories with total sales of $97.1 million (a 76-percent increase).

E-commerce platforms have also continued to expand beyond COVID-19 restrictions and supply chain shortages in brick-and-mortar outlets. Growth has not just been limited to food delivery services, such as PedidosYa, Rappi, and Cornershop. Major supermarket chains Santa Isabel (Cencosud) and Unimarc also launched e-commerce platforms in 2020 and 2021. Euromonitor sources indicate that Chilean food and drink e-commerce sales rose by 55 percent in 2021 to $1.8 million, and are expected to continue rising.

Prospects for U.S. Agricultural Exports

Despite the high-quality reputation of U.S. brands in Chile, several primary agricultural exports, including pork and beer, lost market share in 2021. However, total U.S. agricultural exports to Chile still increased by 29.5 percent ($1.27 billion) in the same year, indicating that significant expansion opportunities remain in the Chilean import market. The U.S. OAA in Santiago indicates that there is still a lack of awareness among Chilean consumers and importers as to the variety and quality of U.S. products, specifically for premium beef cuts and cheeses. Additionally, competition from Mercosur (particularly Brazil, Paraguay, and Argentina) remains high for consumer-oriented products.

Processed Pork Products

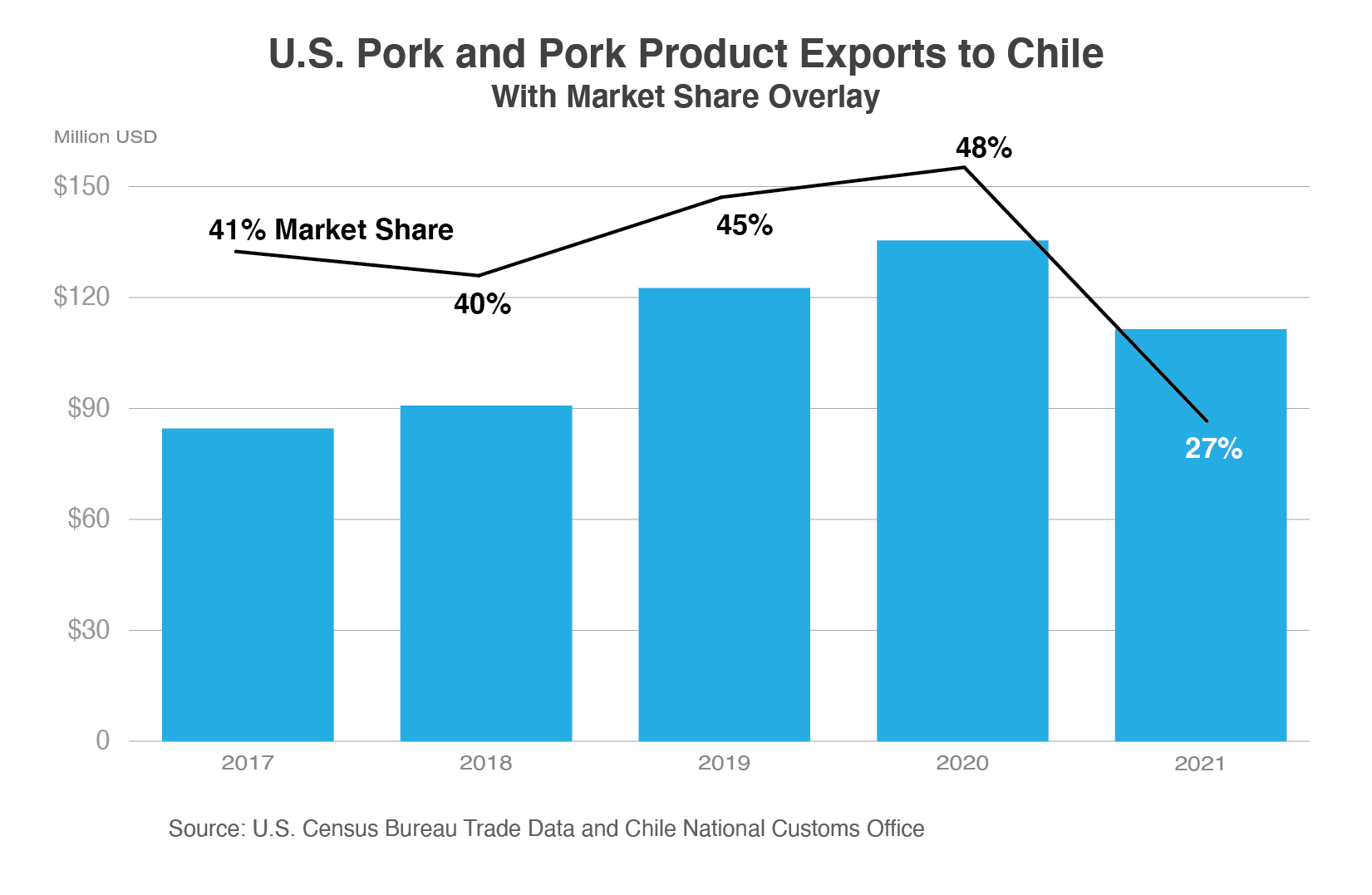

According to Chilean National Customs data, the country imported $423 million worth of pork and pork products in 2021. During the same year, United States pork exports to Chile contracted to $111 million from a high of $135 million in 2020. This 18-percent decline can be partly attributed to a significant increase in pork imports from the EU (especially Germany, Spain, and Poland). In 2021, the EU held 33 percent of the Chilean pork import market share compared with just 12 percent in 2020. Brazilian imports have stayed consistent, comprising 36 percent of Chilean pork imports in 2021. The U.S. OAA in Santiago indicates that U.S. pork cuts remain competitive against Brazilian suppliers, and processed U.S. pork products offer an opportunity to expand sales beyond commodity pork.

Premium Beef Cuts

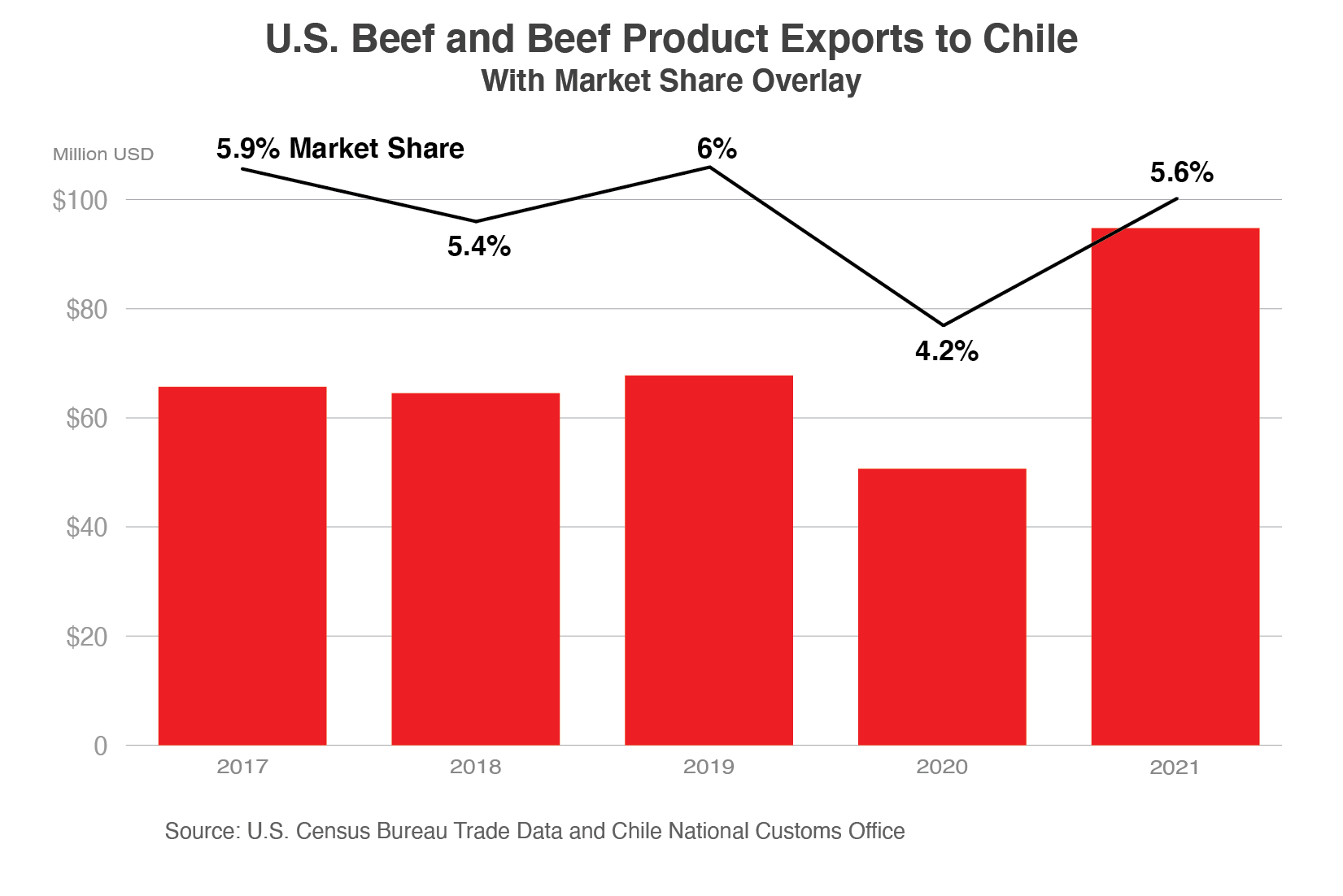

Domestic beef production is insufficient to meet Chilean demand, and low-cost Argentinian, Brazilian, and Paraguayan beef comprise the majority of beef imports. These products are generally lower quality, leaving a market opportunity for premium U.S. beef cuts. Consumers perceive U.S. beef as high quality and, with premium products increasingly within the purchasing power of many Chilean consumers, there is room to fill this niche. United States exporters currently hold less than 6 percent of market share in a $1.7 billion beef import market.

Beer and Distilled Spirits

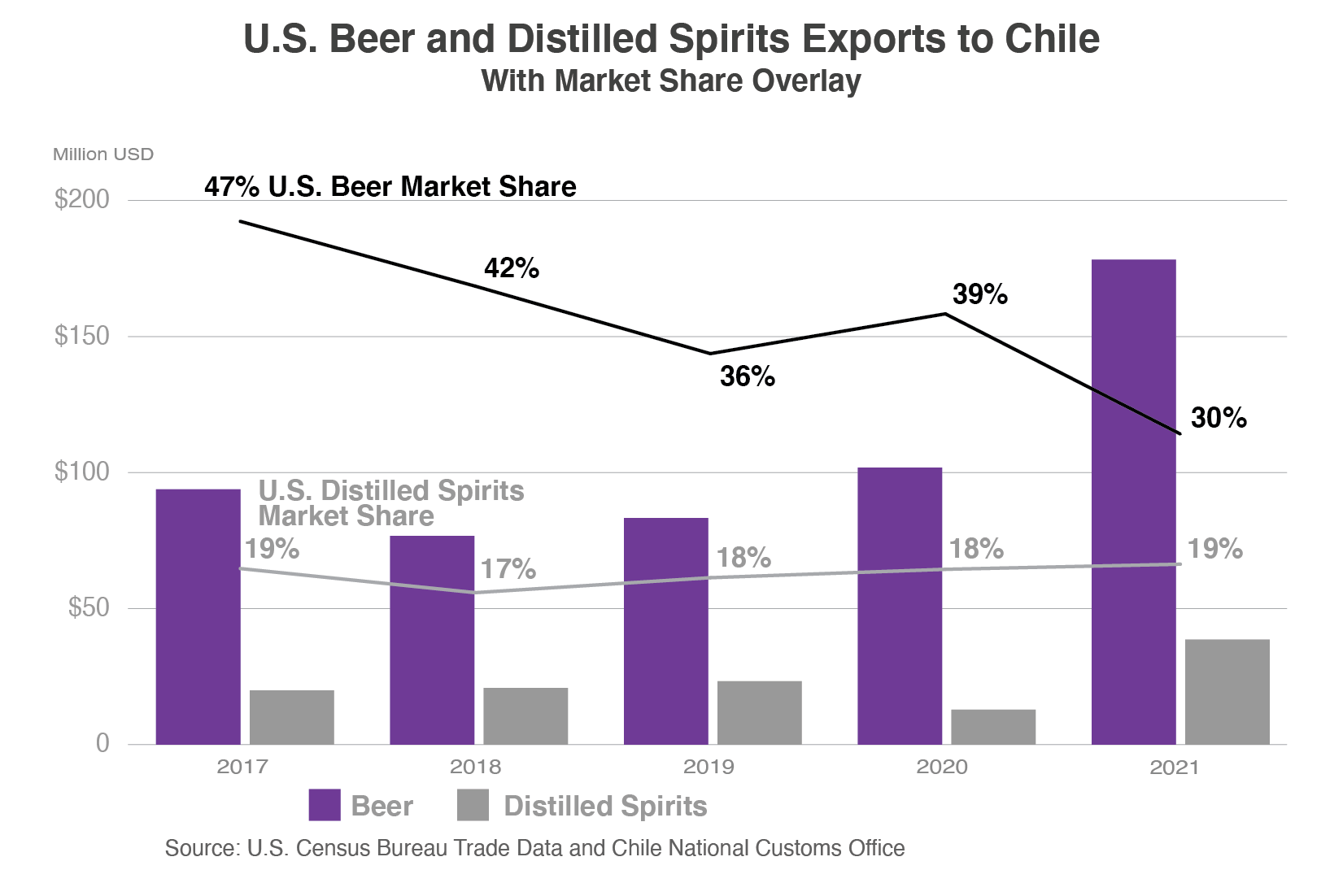

Beer remained among the top five agricultural exports to Chile for the last five years. In 2021, beer exports from the United States reached their highest recorded level, making them the premier U.S. agricultural exports to Chile at $178 million in total exports. Consumer preference leans toward U.S., Mexican, and Belgian beers, although domestic craft beer production is growing. Belgian exporters have become increasingly competitive over the past five years, gaining 10 percent of the Chilean beer import market share by 2021. However, as of February 22, 2022, once a U.S. beer import has been registered with the Alcoholic Beverage Registry, it will no longer need to be tested upon arrival to Chile. This policy change will eliminate the previous biannual testing requirement and increase access to Chilean markets for U.S. beer products.

Distilled spirits sales have maintained consistent growth in both real terms and market share during the last five years. United States distilled spirits exports to Chile center around whisky, with 47 percent of total 2021 export value, and cordials, with 42 percent. Only the United Kingdom holds higher market share at 35 percent, exporting a total of $63.8 million (mostly whisky) compared to the $35.3 million sold by the United States.

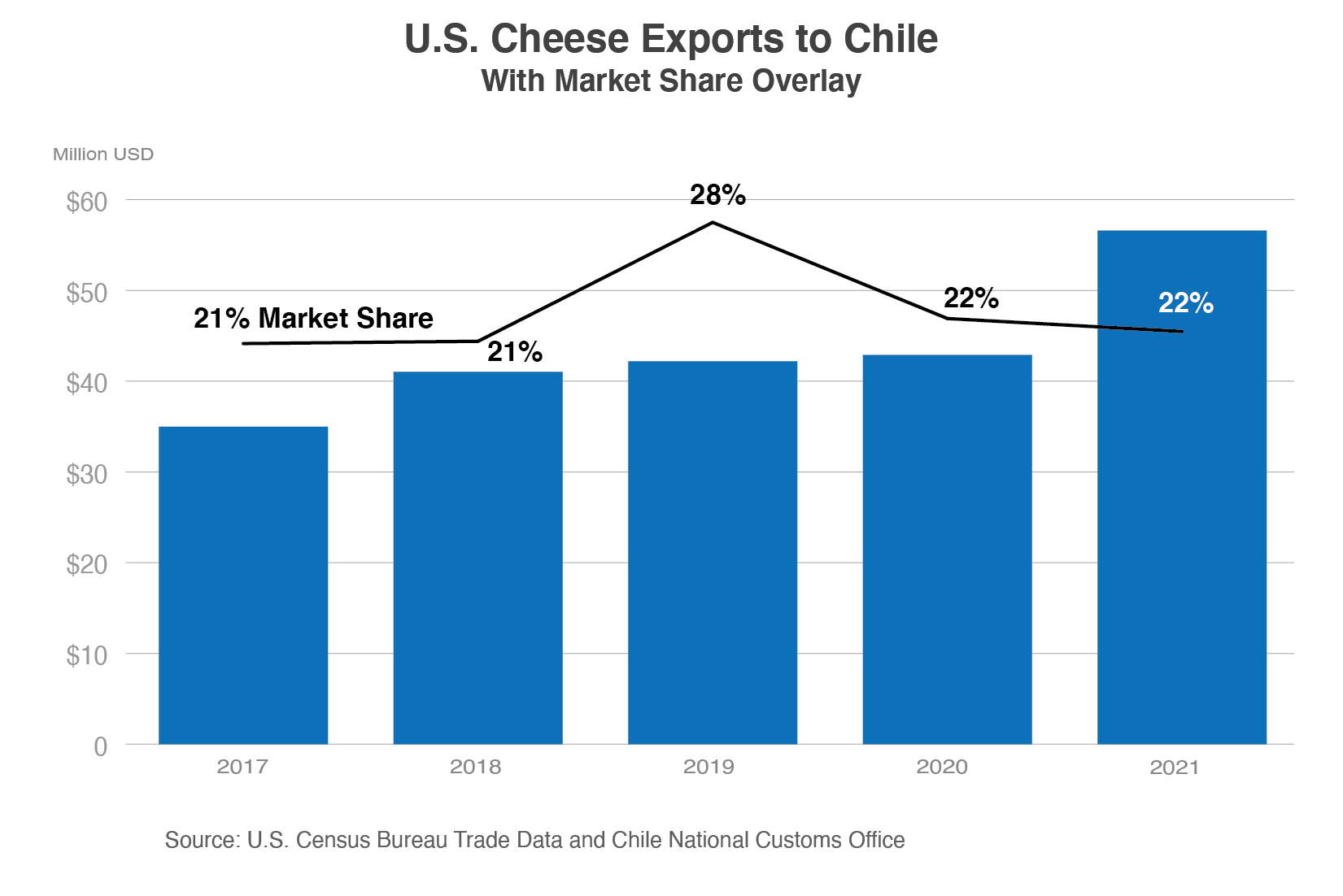

Cheeses

Although Chile’s Oficina de Estudios y Políticas Agrarias reports that domestic cheese production has increased by more than 20 percent year-over-year for the past five years, Chile still relies heavily on cheese imports to supplement its cheese demand. Cheeses comprised 56 percent ($59 million) of all U.S. diary exports to Chile in 2021; total U.S. cheese exports to Chile have increased steadily for the last five years. Argentina is a significant, low-cost competitor due to the benefits of lower production costs and proximity, but its exports are largely limited to gouda and mozarella cheese varieties. United States cheese companies have a history of success in cheddar cheese, which increased in total sales value by 104 percent from 2020 to 2021, and in fresh cheeses including whey and curd, which increased by 34 percent during the same period.

Trade Policy

As of January 2022, Chile has negotiated 30 trade agreements covering 70 markets. It is also an associate member state of Mercosur, which strengthens its ties to the South American trade bloc, particularly Argentina and Brazil. The Comprehensive and Progressive Agreement for Trans-Pacific Partnership and an update to the EU-Chile free trade agreement (FTA) are also pending. However, the U.S.-Chile FTA was fully implemented in 2015, allowing many U.S. exports to enter Chile duty-free.

While trade barriers continue to be eliminated between the two countries, there are a number of technical regulations exporters should consider prior to entering the market, including the Chile Food Labeling and Advertising Law (see pages 16-18, impacto internacional). The regulation affects domestic and imported products, which must adhere to defined limits of sugar, saturated fats, calories, and sodium. The 2019 Dairy Labeling Law (pending implementation) also establishes standards for manufacturing, naming, and labeling of milk products or products derived from milk (including cheese). The law requires producers to specify the country of origin for the raw milk used to manufacture the product, and packaging must be marked with the image of the corresponding flag. The Alcohol Labeling Law defines an alcoholic beverage as any product with an alcoholic content equal to or greater than 0.5 percent. This law requires warning labels about the consequences of the harmful consumption of alcohol as well as the consequences for at-risk populations including pregnant women, motorists, and minors.

Conclusion

Chile remains a competitive market for U.S. exports for good reason. Chilean demand for high-quality products represents the United States’ largest South American consumer-oriented market opportunity. United States exporters of premium products including beer, distilled spirits, pork and pork products, cheese, and beef have operated with success in both the retail and HRI sectors. The combined impact of the economic recovery, the continued easing of barriers to entry for U.S. trade, and a demonstrated demand for high-value U.S. products creates significant and expanding opportunities for exporters seeking to enter the Chilean market. Promotion activities to increase awareness among Chilean consumers and importers as to the variety and quality of U.S. products, specifically for premium beef cuts and cheeses, could further improve prospects for U.S. exporters.

1 Counting the EU-27 as one entity.